The Moderating Effect of Knowledge Stocks Capability on the Relationship Between Business Process Reengineering Factors and Organizational Performance Services Firms

Introduction

The intensive competition in the globalized business world has forced business institutions to make changes their operation processes beyond local competition to global competitiveness. In same manner, according to Goksoy, Ozsoy and Vayvay (2012) if a firm wants to survive in today’s hypercompetitive environment it needs to bring in moderate change every year and undergo a major change almost every fifth years. Thus, to success in this global economy, most of organizations must have a unique strategy and distinctive structure and processes which are fast, high quality, flexible as well as low cost (Khong, 2003). This trend has led many services firms in world to improve their performance flexibility, customer service quality, speed, reduce operating costs and enhance profitability performance to adapting with global changes.

Current challenges in business global environment forced the firms to continue searching and adopting a new management and operations philosophy such as business process reengineering (BPR) and total quality management (TQM).

BPR became one of the popular management approaches in dealing business in extremely fast technological advancement, and any changes or transformation among organization because it helps to improve the performance of companies (Hammer & Champy, 1993). Thus in various industries and services are inspired to get its benefits for business success (Evren & Ayşegül, 2015). According to Sidikat & Ayanda, (2008) apply BPR in organizations led to successful organizational performance.

BPR became one of the popular management approaches in dealing business in extremely fast technological advancement, and any changes or transformation among organization because it helps to improve the performance of companies (Hammer & Champy, 1993). Thus in various industries and services are inspired to get its benefits for business success (Evren & Ayşegül, 2015). According to Sidikat & Ayanda, (2008) apply BPR in organizations led to successful organizational performance.

Many of management researchers describe the BPR is a pioneering attempt to change the way work is performed by simultaneously addressing all the aspects of work that impact performance; including the process activities, the people’s jobs and their reward system, the organization structure and the roles of process performers and managers, plus the management system and the underlying corporate culture which holds the beliefs and values that influence everyone’s behavior and expectations (Cypress, 1994). With BPR, rather than simply eliminating steps or tasks in a process, the value of the whole process itself is questioned (Gotlieb, 1993). According to Goksoy, Ozsoy and Vayvay,( 2012) business process reengineering is one of the management methodologies help the organizations and firms in provide innovative ways, radical changes, fast administrative processes strategic value-added, and systems, policies, organizational structures, information technology and content function and work flow to achieve improvements.

Furthermore, recently the organizational performance assessment is not just based on the financial performance, but also response to change in environment to adapt and interaction with new technology and communication systems and customer needs. Hence, the traditional performance which is mainly on financial point of view is no longer adequate to be used as the only indicator of company’s performance.

Based on central bank of Sudan (CBOS) annuals reports, the Sudanese services firms has great contribute in Sudan GDP about 48% in 2012. Furthermore, the service sector in Sudan comparing with international services business are suffer and have face various challenges and issues such as Poor infrastructure, Lack of funding, and Government regulations plus the global challenges this business complex environment push the Sudanese service sector to research and bring safe business solutions like BPR. Sudanese services sector involve financial intuitions, communication and transport, education, health. One of significant attempts to response to international business change was done after 1997, the Sudanese services firms had embarked upon a liberalization of its financial systems, culminating, in 2000,in adoption of comprehensive management program to banks restructuring(Kireyev,2001).Under the financial sector master plan unveiled by central bank of Sudan (CBOS), the local firms opened to new foreign competitions, that lead liberalization and globalization of business, in addition, consumers are becoming more knowledgeable and demanding. Currently, the service sector in Sudan not only complete locally, but will also set up defensive strategies against mega- global competitors from abroad (Lee, 2006). Foreign competitions one of the main of success factors push the Sudanese services firm to adopting new strategies to enhance organizational performance (efficiency and flexibility).

this study addresses the gaps in the literature by investigating the link between BPR and organizational performance in Sudan context, through the recognition of the range of effect and interrelation of business process reengineering success factors; organizational change, top management commitment, information technology infrastructure, change management systems and culture and management competence.

Business process is expected has direct and direct effect on organizational performance. In addition, the study explores the moderating effect of learning capabilities (knowledge stock and learning flows) on relationship between the reengineering factors and organizational performance.

Literature Review

Business Process Reengineering Concept

Some researchers argue that the original concept of reengineering can be traced back to the management theories of the nineteenth century. Frederick Taylor suggested in the 1880‟s that managers use process reengineering methods to discover the best processes for performing work, and that these processes be reengineered to optimize productivity. BPR is known by many names, such as ‘core process redesign’, ‘new industrial engineering’ or ‘working smarter’. All of them imply the same concept which focuses on integrating both business process redesign and deploying information technology to support the reengineering work.

Business process reengineering exploring how business processes currently operate, and rethinking to how redesign these processes to eliminate the wasted or redundant effort and improve efficiency, and how to implement the process changes in order to gain competitiveness. the BPR seeking to develop new ways of organizing tasks, organizing people and designing information technology systems so that the processes support the organization to achieve its goals (Smith, 1994).

The book “Reengineering the Corporation”: A Manifesto for Business Revolution by Hammer and Champy (1993) is widely referenced by most BPR researchers and is regarded as one of the starting points of BPR. The following is their definition of BPR:

The definition of BPR: the fundamental rethinking and radical redesign of business processes to achieve dramatic improvements in critical, contemporary measures of performance, such as cost, quality, service and speed. (p. 32)

A review of the literature on background of business process reengineering shows that most, of the studies focus on:

A: applicability of business process reengineering critical success factors, methods, models and lessons to the applications and implementation (Hafeez, A. 2003; Alhmaly &Otaibi, 2004; Ahmad Zairi, 2007; Hamid, 2008; Digna,2010; Damanhouri, 2015).

B: the role of information technology in business process reengineering applications in firms (Hammer Champy, 1993; Olalla, 2000; Attaran, 2003; Wu Xiaosong and Li Yijing, 2012; Razalli And Others, 2012; Razalli and Aizat, 2015).

C: the integration between business process reengineering program and other management programs such as, especially relationship between total quality management (TQM) and business process reengineering (Edward and Gore, 1999; Gonsalves, 2002;Saman, 2003).

In general, the majority of studies on business process reengineering have focused on the critical success factors for successful implementation in private business, whereas are few studies have been conducted in services firms.

Therefore, it is risky to generalize the business process reengineering success rate, because the evaluation is subjective as cross national differences (such as cultural believes, norms and core values) may exist. Reengineering is a painful process because the whole set of values and beliefs in the organization are being challenged (Hammer &Champy 1993). BPR factors in the present study have been adapted based on the scope of study and appropriate to the services firms, which is in line with the earlier studies (Al-Mashari & Zairi, 1999; Ahmad et al., 2007). BPR factors are the independent variables, which includes 1) Change Management systems and culture 2) Top Management Commitment, 3) information technology infrastructure, 4) Management competence, 5) organizational change.

Organizational Performance Concept

A variety of definitions exist concerning organizational performance: Organizational performance is a result of the effectiveness and efficiency of the actions that an organization undertakes (Neely, 1999). Slater & Narver (1995) mentioned that performance is reflects an organization’s understanding and knowledge regarding customer needs and expectations. Organizational performance could be linked with market orientation, organization learning, human resource productivity, quality improvement or any other component (Banker & Sinkula, 1999).

Razalli, (2008) found that hotel performance could be improved through good leadership practice and provision of customized service design for select clientele in the service sector. Organizational performance assessment is significant activity due the assessment output very important to stakeholder in or out of organization such as managers, regulators and customers

In non-sustainable environment, Managers are continually face common issue which is how improve their firm’s performance. Resource-based view was used in variety of researches and studies to explain the variance in organizational performance (Wernerfelt, 1984; Barney, 1986; Prahalad & Hamel, 1990). Organizational performance could be linked with market orientation, organization learning, human resource productivity, quality improvement or any other component (Day, 1994; Banker & Sinkula, 1999; Santos-Vijande et al., 2005).

Organizational performance is assessed by the application of financial or both financial and non-financial measures (Venkatraman & Ramanujam, 1986). There are number of studies in the literature that used non-financial measures to evaluate the effectiveness and performance of organization (Quinn & Rohrbaugh, 1983; Venkatraman & Ramanujam, 1986). It is suggested that four models i.e. human relations; internal process; open system and rationale goal model could represent the organizational performance (Quinn & Rohrbaugh, 1983).

Financial indicators, such as return on investment (ROI), earnings per share (EPS) and return on equity (ROE) are used by the number of organizations to measure their progress. Return on investment is used to reflect the profitability while corporate performance was measured by operating cash flows and return.

Knowledge Stocks Concept

The stock of knowledge refers to all that is already known or needs to be known, which includes knowledge as something that individuals, groups or organizations have (knowledge as possession) and do (knowledge as practice). Hence knowledge stocks include knowledge (cognition) and knowing (action) (Cook and Brown, 1999) at the individual level, the group level, and the organizational level (Nonaka and Takeuchi, 1995; Crossan et al., 1999).

Organizational knowledge activities are problem-solving behaviors that lead to enhanced organizational performance (Katila and Ahuja, 2002). A firm engaging in knowledge activities seek to optimal manufacturing methods, superior organizational design, new product /service development (Kim, 1997; Tranfield et al., 2000). .

Organizations need to effectively manage their knowledge, which is a part of organizations intangible resources, to survive and develop in increasingly uncertain and changing markets. The resource-based view emphasizes the firm’s resources as the essential factors of sustaining competitive advantage and enhancing the organizational performance. A number of authors have defined the concept of learning capabilities; to cite for example, Fiol and Lyles, (1985) who expound it as “the process of improving actions through better knowledge and understanding”. Learning is organizational to the extent that, first, it is done to achieve organizational purposes; second, it is shared or distributed among members of the organizations; and third, learning outcomes are embedded in the organizations’ systems, structures, and culture (Snyder and Cummings, 1998). Furthermore, Drucker (1988) believes that knowledge is the only reliable resource of competitive advantage.

Being part of resource based view of firm, Knowledge- based view argues that heterogeneous knowledge bases among organizations and their abilities to create and apply this knowledge, make remarkable differences in organizational performance.

Theoretical Frame Work and Hybothesis Developemnt

Theoretical Base of the Study

The conceptual foundation of this research is mainly drawn from the resource-based view theory (RBV). The RBV is one of the major views in strategic management and attributes superior organizational performance to internal resources (Wernerfelt 1984; Barney 1991).

Strategic resources and capabilities are defined as having the ability to be simultaneously valuable, rare, imperfectly imitable and non-substitutable (Barney, 1991). Furthermore, differences among firms in the resources they choice and stock lead to firm heterogeneity (Barney, 1991). Firm heterogeneity is defined as relatively the differences in strategy and structure across firms in the same industry (Oliver, 1997). These differences lead to variations in firm performance among firms in similar industries(Peteraf, 1993).

Resources include financial, human and technological resources, physical assets and any items that can be considered strengths in a typical strength, weaknesses, opportunities and threats analysis (Bryson, Ackermann and Eden 2007). Resources can be tangible (such as financial resources or physical capital) and intangible (such as human capital, organizational knowledge, organizational culture or organizational networks and relationships).

Propose Study Model and Hypotheses Development

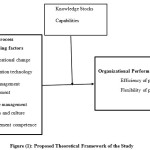

Following the theoretical based of the study, the conceptual framework for this study as shown in figure (1) showed the list of business process reengineering identified and rated in this study and proposes link of process reengineering factors to organizational performance. The theoretical framework of the study proposes that learning capabilities has moderating effects on relationship between process reengineering factors and firm organizational performance.

The study model in figure (1) is based on the theory analysis resources, the resource‐based view (RBV), which states: effective and efficient application of all useful resources that the company can muster helps determine its competitive advantage (Wernerfelt, 1984).

The Moderating Effects of Knowledge Stocks on the Relationship Between Organizational Performances.

The RBV suggest that firms with valuable, rare, and inimitable resources have the potential of achieving superior performance (Barney, 1991). Knowledge-based resources is part RBV theory. It define is considered particularly important for providing competitive advantage (Grant, 1996; Spender, 1996), and learning processes are thus necessary to transform and refine a firm’s knowledge resources in accordance with the environmental conditions. This link between knowledge and learning processes is often associated with the organizational capability to learn (Crossan et al., 1999; Sanchez, 2001). The knowledge-based view of the firm, which emerges as an extension of the resource-based view of the firm, argues that heterogeneous knowledge bases among firms, and the ability to create and apply knowledge, are the main determinants of performance (Grant, 1996). The analysis shows the positive some relevant insights link existing between: learning capability and non-financial performance; and non-financial performance and financial performance (Revilla, 2006). The reengineering experts and Practitioners recommended to fully and successfully implementation business process reengineering in organizations should be taken in account some factors challenges such as organizational culture which is one of the keys challenges faced by organizations when applying reengineering is the willingness to change, which is one of the critical factors in the success of the application reengineering so organizations need to change the organizational culture of the old to the new culture based on a change in the principles, values and concepts and beliefs to suit the principles reengineering (Al-Otaibi, 2009). Terziovski, Fitzpatrick and O’ Neill (2003) believed that must change attitudes of individuals and organizational culture when applying reengineering and to reduce staff resistance to change. According Maaytah (2010) that the resistance to change of reengineering customary when individuals in order to protect their positions, so management must attention to training and education to create a culture of openness to change, knowledge and creativity, and accept the challenge in the work and composition of the teams, and the delegation of authority, and give freedoms, and policy change and according Tayfur (2006), it has to be the creation of an organizational culture when applying reengineering rely on instilling the values and positive attitudes towards certain principles, including: improving governance and deepen the spirit of commitment, and encourage creativity teamwork and spread the spirit of the team, and take responsibility and control, and spread the spirit of challenge and the desire to achieve it. Thus, this research suggest that the organizational performance is has been effected by business process reengineering across the learning capabilities; knowledge stocks and learning flows. Many of researches and studies conducted to investigating significant of moderating effect of learning capabilities as moderator factor but there (based on researcher information extend) are an empirical examination of such a relationship was not found in the literature. The positive impacts of learning capabilities have also been studied previously, but the studies often focus only on the positive impacts of learning capabilities on firm performance (Isabel, 2006).

Knowledge stocks capabilities moderates the relationship between business process reengineering and firm performance. The past studies focusing on the business process reengineering and organizational performance relationship provide a significant insight of successful and full implementation of business reengineering resulting in increased organizational performance (Hammer &shampy, 1993; sidikat, 2010). However, there is a lack of studies investigating the moderating effect of learning capabilities in the relationship between business process reengineering and organizational performance. The positive impacts of learning capabilities have also been studied previously, but the studies often focus only on the positive impacts of learning capabilities. Many of theoretical and empirical progress has also been made from the knowledge management literature in identifying the direct link between knowledge stocks and firm performance (Choi and Lee, 2003; Chuang, 2004).

Based on some of studies and researches findings there is positive relationship and essential role between business process reengineering and knowledge stocks capabilities through the education and training plan to facilitate the reengineering project in business organization (Alotabi, 2006; Al-Baghdadi and others, 2008).

Furthermore, previous studies focusing on role of knowledge stocks capabilities in business process application rather than considering knowledge capabilities in as a moderator in the relationship between business process reengineering and organizational performance.

Thus, the purpose of this study is to explore the moderating effect of knowledge stocks capabilities on the relationship between business process reengineering and organizational performance in the context of services firms.

Current study suggest in general, there is international consensus the fully and successfully business process reengineering implementation will ultimate to improve the organizational performance. To be successful in implementing business process reengineering, many of the important factors that need to be concerned is to fit the project with organizational culture and information technology. The organizations need to change the organizational culture and work core values according to change the classical management principles, values and beliefs to suit to reengineering project (Al-otaibi, 2006). To ensure the success process change through the business process reengineering the organization must change of individuals and groups attitudes and organizational culture through applying reengineering and to reduce staff resistance to change (Terziovski, Fitzpatrick and O’ Neill, 2003). The Organizations must adopt and sponsor training and education strategic plan to develop new organizational culture to facilitate the business processes reengineering through knowledge stocks capabilities and accept the challenge in the work and composition of the teams, and grand more authorities, and work decision share (Tayfur, 2006). On other hand, the knowledge-based view of the firm is a recent theory to interpreter the link between firm capabilities and organizational performance. Specifically, this method suggests that knowledge accumulation may be the source of superior performance. Knowledge stocks capabilities is also considered to enhance the organizational performance.

A study by Donna Marie De Carolis and David L. Deeds (1999) found the relationship between stocks and flows of organizational knowledge and firm performance in the biotechnology industry. Also suggest that a firm’s geographic location, alliances with other institutions and organizations and R&D expenditures are representative of knowledge flows, while products in the pipeline, firm citations and patents are indicative of knowledge stocks.Thus, the following two main hypothesis can be formulated:

The effect of business process reengineering on efficiency of performance is stronger when Knowledge stocks are higher.

H1.1 The effect of organizational structure on efficiency of performance is stronger when Knowledge stocks are higher.

H1.2 The effect of IT infra-structure on efficiency of performance is stronger when Knowledge stocks are higher.

H1.3 The effect of change management systems and culture on efficiency of performance is stronger when Knowledge stocks are higher.

H1.4 The effect of top management commitment on efficiency of performance is stronger when Knowledge stocks are higher.

H1.5 The effect of management competence on efficiency is stronger when Knowledge stocks are higher.

According to Chaiporn Vithessonthi (2011), there is the moderating effect of knowledge capabilities on relationship between Strategic change and firm performance. Lee and Kim (2015) were discovered that the type of strategic alliance through knowledge capabilities, leads to a more flexibility, and consultative management style. Based on the above, the hypothesis is as follows:

H2. The effect of process reengineering on flexibility of performance is stronger when Knowledge stocks are higher.

H2.1 The effect of organizational structure on flexibility of performance is stronger when Knowledge stocksare higher.

H2.2 The effect of IT infra-structure on flexibility of performance is stronger when Knowledge stocksare higher.

H2.3 The effect of change management systems and culture on flexibility of performance is stronger when Knowledge stocksare higher.

H2.4 The effect of top management commitment on flexibility of performance is stronger when Knowledge stocksare higher.

H2.5 The effect of management competence on flexibility of performance is stronger when Knowledge stocksare higher.

Research Methodology

Variables

Independent Variables

The independent variables of the study are business process reengineering factors; top management commitment, organizational change, change management commitment, information technology infrastructure and management competence. Each of these variables was measured by a five-point Likert-type scale, ranging from

(strongly disagree) to 5 (strongly agree)

A neutral response – “neither disagree nor agree” – was adopted to reduce uninformed responses. Whenever possible, established scales were utilized. When the items had to be modified, the items were derived from the literature.

Moderator Variable

There was no comprehensive scale on which to measure knowledge stocks capability, therefore the items used had to be developed first. The items were rooted in literature. The moderator variable was measured by seven items. A five-point Likert-type scale, ranging from 1 (strongly disagree) to 5 (strongly agree), was utilized.

Dependent Variable

The dependent variable: organizational performance. Based on previous literature, the domain performance was measure by efficiency (financial) and flexibility (nonfinancial). The respondents were asked to evaluate the efficiency and flexibility (ROA, ROI, market share, quality, speeds, etc.) performance of the firm within the past three years on a scale of 1 (much worse) to 4 (excellent).

Control Variables

A total of four control variables were suggested: three control variable were adopted firm size (measured by number of employees in the firm), owner form (government and private and age of business (less than 10 years and over the 10 years).

Sample and Data Collection

The research setting was a cross-sectional study design. It involves gathering the data only once or at one point in time to meet the research objectives (Cavana, Dalahaye, & Sekaran, 2001). The advantage of using a cross-sectional study is that it is economical and does not take time like a longitudinal study. The majority of the previous studies on BPR used case study descriptive research design (O’Neil & Sohal, 1999). The data from this study was gather from general manager, director, managers and head of departments that represent the respective services firms in Sudan. Present study, attempts were made to increase the response rate such as by reminding the respondents through telephone call, SMS and self-visit (Sekaran, 2006). As a result of this efforts, 200 questionnaires responded by the firms were returned out of the 221 questionnaires distributed by hand delivery to the respondent firms (finance, communication and education) in Sudan. This makes the response rate of 89.14% based on the definition of response rate (Jobber, 1989). Out of these 200 responses collected, 181 questionnaires were useable for further analysis making a valid response rate of 89.0%. This response rate is considered adequate considering that, according to Sekaran, (2006) the response rate of 30% is acceptable for surveys.

To check for non-response bias, an analysis of variance (ANOVA) test was performed. The informants were divided into four groups: the first informants, the first follow-ups, and the last follow-ups. The results of the ANOVA test revealed that there was no significant difference (at the 5 percent significance level) between the two groups. The results did not reveal any bias in the sample.

Validity and Reliability of the Measures

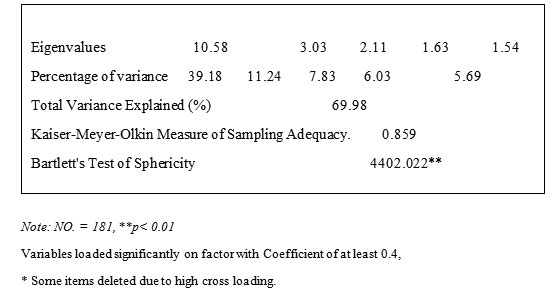

All study dimensions and constructs were tested for validity and reliability to ensure the consistency. Cronbach’s alpha coefficient is widely used as a measure the reliability of the study dimensions. Factor analysis was conducted to measures the construct validity. Factor analysis was conducted on study items, which was used to measure study variables constructs. Table ( ) show the summary of results of factor analysis on study variables constructs; business process reengineering, organizational performance and knowledge stock. All study variables components/factors loaded with eigenvalues exceeding 1.0. All the remaining items also had the factor loading values above the minimum values of 0.50, with value of cross loading less than .50.

Validity of Business Process Reengineering Factors

The table (1) shows that the items for business process reengineering factors loaded on five components/factors with eigenvalues exceeding 1.0. These three factors explain 69.9% of variance in the data (above the recommended level of 0.60). All the remaining items also had the factor loading values above the minimum values of 0.50, with value of cross loading less than .40. The first factor of business process reengineering variables organizational change (8) items. Thus, the name original name of this factor was retained as it is, and factor two information technology infrastructure (5) items. Concern to the third factor is change management systems and culture

(6) Items. Further, the name original name of this factor was retained as it is. And then the factor four management competence (3 items). Also this factor was retained as it is. Whereas process reengineering project management (4 items). Was renamed to top management commitment based on literature review.

As shown in Table (1), factor loading of business process reengineering variables items on the five factors ranged from 0.559 to 0.810. Thus, this study found that business process reengineering in Sudanese services firms consists of five factors, namely; Organizational change, Information Technology Infrastructure, top management commitment, change management systems and culture and management competence.

Table :1 Rotated Factor Analysis for Business Process Reengineering Factors

|

Rotated Component Matrixa

|

|

|

Component

|

|

1

|

2

|

3

|

4

|

5

|

|

F4_our firm try to merage the mgt stratigic process change

|

.830

|

.117

|

.209

|

.165

|

.077

|

|

E5_flexibile organizional strucure

|

.826

|

.113

|

.216

|

.164

|

.063

|

|

E4_clear organizional strucure

|

.798

|

.151

|

-.063

|

.238

|

.152

|

|

F3_our firm has BPR conslatants

|

.796

|

.154

|

-.052

|

.210

|

.148

|

|

F1_our firm has aclear change plan aliging to stratic plan

|

.752

|

.133

|

.086

|

.091

|

.129

|

|

F2_our firm has clear vistion to process change

|

.679

|

.266

|

.225

|

.244

|

.111

|

|

E1_top mgt support team work

|

.577

|

.342

|

.244

|

.081

|

.139

|

|

E3_clear task and work

|

.568

|

.417

|

.090

|

.297

|

.002

|

|

d4_IT support the work development

|

.271

|

.792

|

.134

|

.142

|

.225

|

|

d1_deasly useage of IT

|

.249

|

.775

|

.182

|

.096

|

-.056

|

|

d3_IT support doing the work

|

.107

|

.771

|

.229

|

.057

|

.208

|

|

d2_easly access to info.

|

.258

|

.729

|

.184

|

-.023

|

.061

|

|

d6_modern IT

|

.147

|

.728

|

.218

|

.143

|

.039

|

|

c4team work

|

.067

|

.168

|

.822

|

.082

|

.114

|

|

c3_innivation and creatives

|

.227

|

.151

|

.802

|

.085

|

.090

|

|

c2_more autherities

|

.091

|

.245

|

.740

|

-.028

|

.041

|

|

c5_share in decition made

|

.191

|

.034

|

.717

|

.127

|

.174

|

|

c6_proads change culure

|

-.056

|

.424

|

.609

|

.298

|

-.010

|

|

c1_motovate

|

.132

|

.409

|

.538

|

.250

|

.150

|

|

c7_training plan

|

.045

|

.357

|

.517

|

.458

|

.070

|

|

F5_in our firm the process change aliging to stratigic plan

|

.228

|

.153

|

.025

|

.880

|

.082

|

|

E6_adminstartion based on top mgt

|

.228

|

.150

|

.093

|

.867

|

.144

|

|

F6_our firm has clear objectives from process redisgn

|

.373

|

.023

|

.264

|

.732

|

.160

|

|

E7_accordaion among depts

|

.397

|

.041

|

.254

|

.730

|

.176

|

|

G2_top mgt in our firm has agood belevies to process change through BPR

|

.072

|

.126

|

.093

|

.154

|

.876

|

|

G1_firm leaders has agood visitions to change mgt.

|

.191

|

.096

|

.132

|

.195

|

.860

|

|

G3_top mgt in our firm has agood process change program

|

.364

|

.129

|

.240

|

.061

|

.617

|

Validity of Organizational Performance

The table (2) shows that the items for organizational performance variables loaded on two components/factors with eigenvalues exceeding 1.0. These three factors explain 68.24% of variance in the data (above the recommended level of 0.60). All the remaining items also had the factor loading values above the minimum values of 0.50, with value of cross loading less than .40. The first factor of organizational performance variables is efficiency (4) items. Thus, the name original name of this factor was retained as it isand factor two flexibility four items. However, the name original name of this factor was retained as it is.

As shown in Table (2), factor loading of organizational performance variables items on the two factors ranged from 0.559 to 0.810. Thus, this study found that organizational performance in Sudanese services firms consists of two factors, namely; efficiency and flexibility.

Table 2: Rotated Factor Analysis for Organizational Performance

|

Organizational performance efficiency

in last three years our firm has achieved:

|

Component

|

|

1

|

2

|

|

PI2_Return on sales (ROS).

|

.913

|

.270

|

|

PI3_Return on investment (ROI)

|

.903

|

.315

|

|

PI1_Profit margin (EPS).

|

.893

|

.339

|

|

PJ1 _ Good market position.

|

.854

|

.357

|

|

Flexibility

|

|

|

|

PK1_ Reducing the time for market acceptance of our services.

|

.326

|

.856

|

|

PK2_increasing the speed at which we respond to customer requests

|

.316

|

.828

|

|

PK3_Tracking customer trends.

|

.387

|

.817

|

|

PK4_improving our relationships with our customers.

|

.186

|

.743

|

|

Eigenvalues 5.46 1.16

|

|

Percentage of Variance Explain 68.24 14.51

Total Variance Explained (%) 82.75

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. 0.897

Bartlett’s Test of Sphericity Approx. Chi-Square 1426.289**

|

Note: NO. = 181, **p< 0.01

Variables loaded significantly on factor with Coefficient of at least 0.5.

Validity of Knowledge Stocks Capabilities

Factor analysis was done on eight items which measures knowledge stocks capabilities

Table (3). Summarizes the results of factor analysis. Table (3) show that all assumptions for factor analysis have been fulfilled, namely, KMO (.867), Bartlett’s test of sphericity (p=.00), communalities (>.50), eigenvalue (>1), and factor loading (>.50). The factor cumulatively explains 75.297% of data variance. In addition, factor loading for the eight items ranged from 0.719 to 0.8880. The full SPSS output is attached in Appendix.

The results of factor analysis split the learning capabilities items between two factors knowledge stock (six items) and learning flows (two items).

Table 3: Rotated Factor analysis of knowledge capabilities

|

items

|

Component

|

|

1

|

2

|

|

H3_Individuals share knowledge as they work within groups.

|

.880

|

.091

|

|

H6_Policies and procedures guide individual work.

|

.872

|

.086

|

|

H1_Individuals are knowledgeable and qualified about their work.

|

.867

|

.189

|

|

H5_Individuals share knowledge as they work within groups

|

.853

|

.194

|

|

H2_Individual lessons learnt are exchanged within their work group.

|

.773

|

.297

|

|

H4_Individuals are aware of critical issues that affect their work.

|

.719

|

.361

|

|

Eigenvalues 4.75 1.28

Percentage of Variance Explain 59.43 15.97

Total Variance Explained (%) 75.40

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. 0.76

Bartlett’s Test of Sphericity Approx. Chi-Square 1862.58**

|

Note: NO. = 181, **p< 0.01

Variables loaded significantly on factor with Coefficient of at least 0.5.

Reliability of the Measures

Reliability is an assessment of the degree of consistency between multiple measurements of variables (Haire et al., 2010). Cronbach’s alpha coefficient is widely used to assess the internal consistency of the items. Table (5.6) shows the results of the reliability test. According to Nunnally (1978) scale items should have an alpha values greater than 0.60 are to be taken as reliable and demonstrate internal consistency. According to Haire et al. (2010) argued that a Cronbach’s alpha of 0.6 and above was considered an effective reliability for judging a scale. The generally agreed lower limit for Cronbach’s alpha may decrease to 0.60 in exploratory research (Hair et al., 2010). The alphas for all the scales in this study are listed in Table (5.6) explain all items in present study exceeded 0.70. Confirmed that all the scales display satisfactory level of reliability (Cronbach’s alpha exceed the minimum value of 0.6). Therefore, research instrument can be considered to be reliable if the result of the study can be replicable under a similar methodology with stability of measurement over time.The Cronbach’s alpha coefficients of the research instruments are shown in Table (3) (4) (5).

Descriptive Analysis to Business Process Reengineering Factors

Table( 3 ) shows the means and standard deviations of the five components of business process reengineering factors; organizational structure, IT infrastructure, top management commitment, organizational systems and culture and management competencies.

the means and standard deviations of the five components of BPR factors; data Analysis reveals the Sudanese service firms low adopted of reengineering factors the data analysis reveals that the organizational structure (mean=3.06, standard deviation=0.86), followed by top management commitment (mean=2.93. standard deviation=0.97), and then information technology infrastructure (mean=2.9, standard deviation=1.07), and followed by change management systems and culture (mean=2.77, standard deviation=0.93), and the lowest components of five of reengineering competencies (mean=2.74, standard deviation=0.90), Therefore those five dimensions achieved low than an average score of (3.52). Given that the scale used a 5-point scale (1=strongly disagree, 5=strongly agree), it can be concluded that Sudanese service firms are lowly adopted factors of business process reengineering.

Table 3: Descriptive Analysis Of Business Process Reengineering Factors

|

Variables

|

Mean

|

Standard Deviation

|

No of items

|

Cronbach’salpha

|

|

Organizational Structure

|

3.06

|

0.86

|

8

|

0.92

|

|

Information Technology Infrastructure

|

2.90

|

1.07

|

5

|

0.89

|

|

Top Management Commitment

|

2.93

|

0.97

|

7

|

0.88

|

|

change management systems and culture

|

2.77

|

0.93

|

4

|

0.92

|

|

Management Competencies

|

2.74

|

0.900

|

3

|

0.82

|

Note: All variables used a 5-point likert scale (5= strongly agree, 1= strongly disagree)

Descriptive Analysis of Organizational Performance

Table (4) shows means and standard deviations values of the two dimensions of organizational performance. The mean and standard deviations results the Sudanese service firms emphasized more on efficiency of performance (Mean=2.74, Standard Deviation=1.29) followed by flexibility of performance (mean=2.71, Standard Deviation=1.08). Given that the scale (Likert scale) used a 5-point scale it can be concluded that Sudanese services firms (sampled firms) in during the last three years achieved low organizational performance in term efficiency of performance compare with the average mean.

Table 4: Descriptive Analysis of Organizational Performance

|

Variables

|

Mean

|

Standard Deviation

|

No of items

|

Cronbach’salpha

|

|

Efficiency

|

2.74

|

1.29

|

|

0.96

|

|

Flexibility

|

2.71

|

1.08

|

4

|

0.89

|

Note: All variables used a-5 point Likert scale with (5= much better, 1= much worse)

Descriptive Analysis of Learning Capabilities

Table ( ) presents means and standard deviations values of Knowledge stocksThe result of descriptive analysis of learning show the Sudanese services firms emphasized more on Knowledge stocks (mean=2.6, Standard Deviation =0.99). Given that the scale used a 5-point scale it can be concluded that Sudanese services firms have lowly learning capabilities oriented above the average mean.

Table 5: Descriptive Analysis Of Learning Capabilities

|

Variables

|

Mean

|

Standard Deviation

|

No of items

|

Cronbach’salpha

|

|

Knowledge stocks

|

2.6

|

0.99

|

6

|

0.93

|

Note: All variables used a-5 point Likert scale with (5= much better, 1= much worse)

The Moderating Effects of Knowledge Stocks Capabilities

The hypotheses hypothesis of study suggest that knowledge stocks capabilities moderate the relationship between business process reengineering factors and organizational performance.

To test these hypotheses a four-step hierarchical regression analysis was conducted. Hierarchical regression or moderator regression has been suggested by many authors as statistical technique for analyzing the moderating effect (Baron & Kenny, 1986; Sharma et al., 1981; Frazier et al., 2004). In this study, three levels of significance (1%, 5% and 10%) were used to detect the moderating effect of learning capabilities on the relationship between business process reengineering and organizational performance. Arnold & Evans (1979) suggested that the hierarchical regression analysis provides an unambiguous conclusion with regard to the existence of moderator effects. To test the moderator effect a three (3) step hierarchical was conducted to determine what proportion to the variance in a particular variable is explained by other variables when these variables are entered into the regression analysis in a certain order.

In the first step, the control variables are entered, in the second step the predictor variables entered in the regression equation. In the third step, moderating variable was entered into the regression equation to test its isolated effect on the criterion variable.While in step four, the process requires the introduction of a multiplicative interaction term into the regression equation. Accordingly, four multiplicative interaction terms were created by multiplying the values of business process reengineering factors by the values of hypothesized learning capabilities.

To demonstrate if the moderator effect is present on the proposed relationship, three maximum conditions were used. First, the final model is significant. Second, the F change is significant. Third multiplicative interaction term is also statistically significant. Additionally, in order to establish whether moderator is a pure or a quasi-moderating this research applied the criteria mentioned by Sharma et al (1981). If the coefficients of both the multiplicative interaction term and the moderator variable are significant, the moderator is a quasi-moderator. However, if the coefficient of the multiplicative interaction term was significant and the coefficient of the moderator variable effect was not significant, the moderator is a pure moderator. A pure moderator effect implies that the moderator variable (learning capabilities) modifies the relationship between the predictor variable (business process reengineering factors) and criterion variable (organizational performance).

On the other hand, in order to illustrate the nature of moderator effect, a graphical representation was carried out for each significant effect. This process was carried out for testing the moderating effect of knowledge stocks capabilities on the relationship that link the five components of business process reengineering factors (organizational change, information technology infrastructure, top management commitment, organizational systems and culture and management competence ) with the four organizational performance (efficiency and flexibility).This study also splits each component of business process reengineering factors and learning capabilities into two groups (low, high) by using percentiles to see how the moderator has change the relationship.

The Moderating Effect Of Knowledge Stocks On The Relationship Between Business Process Reengineering Factors And Organizational Performance

At first, the results of its direct and moderating effects of knowledge stocks on the relationship between business process reengineering factors and organizational performance, are as follows:

The Moderating Effect Of Knowledge Stocks On The Relationship Between Business Process Reengineering Factors And Efficiency Of Performance

Table (6) summarized the results of moderating effect of knowledge stocks on the relationship between business process reengineering factors and performance efficiency. This table helps to assess the statistical significance of the results

The results showed that the F change was significant in all four steps. The results showed that the knowledge stocks moderates the relationship between three components of business process reengineering factors. In model and table the term organizational change 🙁 ß= 1.426, p<0.01). Has a negative and significant effect on relationship between BPR factors and efficiency of performance, whereas the effect is significant and positive when it is moderated by knowledge stocks. Further, the model reveal an interest result in term top management commitment (ß= -0.910, p<0.05) has a positive and significant effect on relationship between BPR factors and efficiency of performance, whereas the effect is still significant but it is negative when it is moderated by knowledge stocks. In addition, the introduction of the interaction terms in step four increase R square about 3% and the model as a whole is significant.

This implies that the model (model 4) was able to explain 59.6% (expressed as a percentage, multiply by 100, by shifting the decimal point two places to the right). However, knowledge stocks show moderating effect of remaining reengineering factors were not significant namely; information technology infrastructure, change management systems and management competence on efficiency of performance. Further inspection reveals that the coefficient of the knowledge stock effect was not significant, which indicate that it is a pure moderator (full interaction).

Table 6: Effect of knowledge stocks on the Relationship between business process reengineering factors and Efficiency of Performance

|

Variables

|

DV: Efficiency

|

|

Step1

Std. Beta

|

Step2

Std. Beta

|

Step3

Std. Beta

|

Step4

Std. Beta

|

|

Control variables:

Owner form

Number of employees

Business age

|

0.303***

-0.458***

-.110*

|

0.157**

-0.234***

-.084

|

.147**

-.207***

-.075

|

.113*

-0.205***

-.065

|

|

predictor variables:

Organizational change

Information technology

Top management commitment

change management systems and culture

Management competence

|

|

0.107*

0.042

0.147*

0.273***

0.101*

|

0.082

0.053

0.179

0.206

0.043

|

-0.607**

0.275

0.689***

0.338*

-0.004

|

|

Moderator variable

Know

|

|

|

0.173**

|

0.051

|

|

Interaction terms:

Korg

Kinfotech

Ktopmgt

Ksyschang

kmgtcomptence

|

|

|

|

1.426***

-0.313

-0.910**

-0.194

0.057

|

|

F value

R²

Adjusted R²

R² change

F change

|

33.089***

0.559

0.348

0.359

33.089***

|

25.832***

0.546

0.525

0.186

14.120***

|

24.444***

0.563

0.540

0.017

6.624**

|

17.471***

0.596

0.562

0.033

2.711**

|

|

Note: Level of significant: , *p<0.10**p<0.05, ***p<0.01

|

The Moderating Effect of Knowledge Stocks on the Relationship Between Business Process Reengineering Factors and Flexibility of Performance

Table (7) summarized the results of moderating effect of knowledge stocks on the relationship between business process reengineering factors and flexibility of performance. The data in the table indicates an interesting results disclosed that the F change was significant in all four steps, implies the four model are significant. The results also show that the knowledge stocks moderate the relationship between just. The introduction of the interaction terms in step four increase R square about 5% and the model as a whole is significant. On other hand, knowledge stocks show no moderating effect between rest components of business process reengineering; information technology infrastructure, change organizational systems and culture and management competence on efficiency. More inspection reveals that the coefficient of the knowledge stock effect was significant, which indicate that it is a quasi-moderating.

Table 7: Effect of knowledge stocks on the Relationship between Business Process Reengineering Factors and Flexibility of Performance

|

Variables

|

DV: Efficiency

|

|

Step1

Std. Beta

|

Step2

Std. Beta

|

Step3

Std. Beta

|

Step4

Std. Beta

|

|

Control variables:

Owner form

Number of employees

Business age

|

.337***

-0.402***

-0.066

|

.171**

-0.187**

-0.041

|

.154**

-0.142**

-0.026

|

.144**

-0.168**

-0.015

|

|

predictor variables:

Organizational change

Information technology

Top management commitment

change organizational systems and culture

Management competence

|

|

0.148*

0.231**

0.012

0.158**

0.128**

|

0.188**

0.167**

0.067

0.045

0.029

|

-0.109

0.049

0.203

0.744***

0.012

|

|

Moderating variable

Know

|

|

|

0.296***

|

0.743**

|

|

Interaction terms:

Korg

Kinfotech

Ktopmgt

Ksyschang

kmgtcomptence

|

|

|

|

0.565

0.323

-0.205

-1.466***

-0.007

|

|

F value

R²

Adjusted R²

R² change

F change

|

26.542***

0.310

0.299

0.310

26.542***

|

21.838***

0.504

0.481

0.194

13.426***

|

23.536***

0.553

0.530

0.049

18.920***

|

18.426***

0.608

0.575

0.055

4.675***

|

|

Note: Level of significant: , *p<0.10**p<0.05, ***p<0.01

|

|

|

Discussion

The Moderating Effects Of Knowledge Stocks On The Relationship Between

Business Process Reengineering And Organizational Performance

The first sub-section discussed the moderating effect of the first dimensions of learning capabilities (knowledge stocks). The results reveal that knowledge stocks moderating the relationship between business process reengineering and organizational performance these results are discussed in more details below:

The Moderating Effects of Knowledge Stocks on the Relationship Between Business Process Reengineering and Efficiency

The results showed that the knowledge stocks a pure moderator (full interaction) the relationship between three components of business process reengineering factors; top management commitment, organizational change and change management systems and culture. The firms which were full successfully implementing of process re-engineering factors (top management commitment, organizational change) with a high knowledge stocks was found positively influencing efficiency at high levels of knowledge stocks. This finding indicates that top management commitment has both a direct and indirect significant effect on the organizational performance of firms. The indirect effect is via knowledge stocks capabilities. The findings concurs with other previous studies which confirm that firms that have flexible management and clearly work values would have a high learning capabilities that would ultimate to a higher level of organizational performance. In addition this study findings in line with empirical a study has been conducted on the knowledge management literature in identifying the direct link between knowledge stocks and firm performance (Choi and Lee, 2003; Chuang, 2004). Furthermore, the study finding consist A study by Donna Marie De Carolis and David L. Deeds (1999) found the relationship between stocks and flows of organizational knowledge and firm performance in the biotechnology industry. Also suggest that a firm’s geographic location, alliances with other institutions and organizations and R&D expenditures are representative of knowledge flows, while products in the pipeline, firm citations and patents are indicative of knowledge stocks.

Further, the study finding in line with a study conducted by Al-Baghdadi And others (2008),the study had try to identify the causes of low efficiency in business organizations and then try to re-engineer its operations through the use of a new entrance in the administration, namely (knowledge stocks management) and was of the most important conclusions that organizations can achieve financial and operational performance of a distinct and competitive position to survival, growth and expansion when taking variables (knowledge stocks management, BPR) and the combined study and attention and regularly and continuously. However, organizations must keep enhancing its knowledge stocks to efficiently and effectively manage reengineering activities.

The Moderating Effects of Knowledge Stocks on the Relationship Between Business Process Reengineering and Flexibility

The results showed that the knowledge stocks moderating the relationship between just one components of business process reengineering; top management commitment. The moderating effect of knowledge stocks on the relationship between change management and organizational performance was in line with a studies conducted by Al-Baghdadi and others (2008), the impact of knowledge management in re-engineering operations of the business. the study had try to identify the causes of low efficiency in business organizations, and then try to re-engineer its operations through the use of a new entrance in the administration, namely (knowledge stocks management) and was of the most important conclusions that emerged from the study: that there is a correlation between knowledge of the phenomenon and the implicit and the BPR. Organizations can achieve financial and operational performance of a distinct and competitive position to survival, growth and expansion when taking variables (knowledge management, BPR) and the combined study and attention and regularly and continuously. On other hand the study finding in same manner with the a study finding by Bengt-Åke Lundvall Peter Nielsen, (2007), The analysis shows that firms that introduce several organizational practices, assumed to characterize the learning organization, are more innovative than the average firm.

Further, the recent of study finding with in line to Ying Liao Jane Barnes , (2015) found there are many studies shows empirical evidence that to build flexibility of organizational performance for long-term competitive advantage, the emphasis should be on developing effective processes to effectively acquire and stocks the knowledge from external and internal the firms.

Directions For Future Research

This study provides some suggestions for future research. The sample from the study is limited to Sudanese service firms. Future research should consider replicating this study in other cultures or countries especially on the moderating effect of knowledge capabilities dimensions. In addition, further research is also, needed to be conducted in other sector or industry besides service sector such as manufacturing, or construction sector. This research would help to generalize the findings of this study in a broader context. Alternatively, a cross-cultural comparative analysis would further enhance the understanding of BPR and learning capabilities of different cultures.

Conclusions

An attempt was made in the present study to investigate the effect of knowledge capabilities on relationship between business process reengineering factors and organizational performance.

This study was conducted among 181 Sudanese large service firms. This study has established from its empirical findings that business process reengineering factors consists of five components (organizational structure, infrastructure of information technology, top management commitment of change, change management systems and work culture and management competence) and can be measured using 35 questionnaire items, which demonstrate internal consistency, its construct validity (factor analysis). The results also found that an important role of knowledge stock capabilities towards competitive advantage and organizational enhancement.

The overall findings from the study have proven that the relationship between business process reengineering factors, knowledge capabilities on organizational performance have been established in the study. This study provides new empirical contribution to academic knowledge and practitioners. To the academia, more research on multi-disciplines need to be conducted to establish the relationship beneficial to the industry and society in general. To the practitioners, the search for organizational performance and competitive advantage should not be dependent on a particular management technique but multiple management initiatives, which are important for survival and success.

References

- Abdul Hafeez, A. 2003. “The Reference for the Application of Scientific Approach Reengineering”, First Edition (Amman: Dar Wael for Publishing and Distribution, 2003).

- Ahmad, H., Francis, A., and Zairi, M. 2007. “Business Process Reengineering: Critical Success Factors in Higher Education”, Business Process Management Journal, Vol.13, No.3, pp.451-469

CrossRef

- Al-Baghdadi, M. A. R. S. (2008). Measurement and prediction study of the effect of ethanol blending on the performance and pollutants emission of a four-stroke spark ignition engine. Proceedings of the Institution of Mechanical Engineers, Part D: Journal of Automobile Engineering, 222(5), 859-873.

CrossRef

- Al-Mashari, M., & Zairi, M. (1999). Business process reengineering implementation processes: an analysis of key success and failure factors. Business Process Management Journal, 5(1), 87-112.

CrossRef

- Al-Otaibi, S. M. 2009. “Re-engineering in the public sector: the critical factors for success”, http://faculty.ksu.edu.sa/salotaibi/DocLib/Forms/AllItems.aspx.\

- Arnold, Hugh J., and Martin G. Evans. “Testing multiplicative models does not require ratio scales.” Organizational Behavior and Human Performance 24.1 (1979): 41-59.Attaran, M. (2004). Exploring the relationship between information technology and business process reengineering. Information & Management Journal, 41(5), 585-596.

CrossRef

- Banker, R., & Kauffman, R. J. (1991). Re-use and productivity in integrated computer-aided software engineering: An empirical study. MIS Quarterly, 15, 374-401.

CrossRef

- Barney, J. B. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99-120.

CrossRef

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research; Conceptual, strategic and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173-1182.

CrossRef

- Bengt-Åke Lundvall Peter Nielsen, (2007),”Knowledge management and innovation performance”, International Journal of Manpower, Vol. 28 Iss 3/4 pp. 207 – 223

- Bryson, J, Ackermann, F & Eden, C 2007, ‘Putting the resource-based view of strategy and distinctive competencies to work in public organizations’, Public Administration Review, vol. 67, pp. 702–717.

CrossRef

- Cavana, R. Y., and B. Delahaye. “l., and Sekaran. U. 2001.” Applied business research: qualitative and quantitative methods.

- Clary, E. G., Snyder, M., Ridge, R. D., Copeland, J., Stukas, A. A., Haugen, J., & Miene, P. (1998). Understanding and assessing the motivations of volunteers: a functional approach. Journal of personality and social psychology, 74(6), 1516.

CrossRef

- Cook, S. And Brown, J.S. (1999), “Bridging Epistemologies: The Generative Dance between Organizational Knowledge and Organizational Knowing”, Organization Science, Vol. 10 No. 3, Pp. 381-400.

- Crossan, M., Lane, H.W., White, R.E. and Djurfeldt, L. (1995), “Organizational learning: dimensions for a theory”, The International Journal of Organizational Analysis, Vol. 3 No. 4, pp. 337-60.

CrossRef

- Cypress, Harold L. “Re-engineering.” OR/MS Today 21.1 (1994): 18-29.

- Damanhouri, 2015. “Factors Affecting The Application Of Business Process Reengineering”, The Journal Of Ayer Vol. 2, 2015- Page 81-97 Issn: 1134-2277

- Day, George S. “The capabilities of market-driven organizations.” the Journal of Marketing (1994): 37-52.

- Dibella, and Nnevis, 1998DiBella, A.J. and Nevis, E.C. (1998), How Organizations Learn. An Integrated Strategy for Building Learning Capability, Jossey-Bass, San Francisco, CA.

- Digna, I. A. 2010. “A Proposed Model for the Business Process Reengineering and Computerization in the Institutions Of Higher Education”, Islamic University, Palestine.

- Drucker, Peter Ferdinand. “The coming of the new organization.” (1988): 45-53.

- Edmondson, Amy, and Bertrand Moingeon. “From organizational learning to the learning organization.” Management Learning 29.1 (1998): 5-20.

CrossRef

- Edward W., Gore Jr., Organizational Culture, TQM. And Business Process Reengineering Anempirical Comparison, (MCB), Journal of Team Performance Management, Vol. (5), No. (5), 1999.

- Evren Ayrancı & Ayşegül Ertuğrul Ayrancı. 2015. A Research on the Relationship between Top Managers’ Intelligence and Their Ideas about Business Process Reengineering: Consideration of Emotionality and Spirituality. International Business Research; Vol. 8, No. 10; 2015 Issn 1913-9004 E-Issn 1913-9012.

- Fiol, C. Marlene, and Marjorie A. Lyles. “Organizational learning.” Academy of management review 10.4 (1985): 803-813.

- Frazier, P. A., Barron, K. E., & Tix, A. (2004). Testing Moderator and Mediator Effects in Counseling Psychology Research. Journal of Counseling Psychology, 51(1), 115-134.

CrossRef

- Goksoy, A., Ozsoy, B., and Vayvay, O. 2012. “Business Process Reengineering: Strategic Tool for Managing Organizational Change an Application in a Multinational Company”, International Journal of Business and Management, Vol. 7, No 2, pp. 89 -112.

CrossRef

- Gonsalves, Geralde, Business Process management: Integration of Quality Management and Reengineering for Enhanced Competitiveness, (PhD), University of Kentucky, United States ± Kentucky, 2002

- Gotlieb, L. (1993), “Information Technology,” Cma Magazine, Vol. 67 No. 2, March, Pp. 9-10.

- Grant, R.M. (1996), “Prospering in dynamically-competitive environments: organizational capability as knowledge integration”, Organization Science, Vol. 7 No. 4, pp. 375-87.

CrossRef

- Hair, JF, Black, WC, Babin, BJ, Anderson, RE & Tatham, RL 2010, Multivariate data analysis, 7th edn, Pearson Prentice Hall, Upper Saddle River, NJ.

- Hamel, G., & Prahalad, C. K. (1990). The core competence of the corporation.Harvard business review, 68(3), 79-91.

- Hamid, S. S. 2008. “The Factors Affecting the Application Of Process Re-Engineering Know-How (Reengineering) Field Study”, Journal Of Accounting, Management And Insurance, No.70, Forty-Seventh Year, Pp. 253-294.

- Hammer, M., & Champy, J. 1993. Reengineering the Corporation: A Manifesto for Business Revolution. The Academy Of Management Review. 19(3): 595-600.

CrossRef

- Hammer, M., And Champy, J.1993. “Information Technology For Management Re-Engineering’s The Corporation: A Manifesta for Business Revolution”, Harper Business, New York, Ny.

- Hammer, M., Champy, J. (1993). Reengineering the Corporation: A Manifesto for Business Revolution. New York: Harper Business

- Hartini Ahmad Arthur Francis Mohamed Zairi, (2007),”Business Process Reengineering: Critical Success Factors In Higher Education”, Business Process Management Journal, Vol. 13 Iss 3 Pp. 451 – 469

- Ingelgard, A. And Roth, J. (2002), “Dynamic Learning Capability and Actionable Knowledge Creation: Clinical R & D in A Pharmaceutical Industry”, the Learning Organization, Vol. 9.No. 2, Pp. 65-77.

- Isabel Ma Prieto Elena Revilla, (2006),”Learning Capability and Business Performance: A Non-Financial and Financial Assessment”, the Learning Organization, Vol. 13 Iss 2 Pp. 166 – 185.

- J.‐C. Spender, (1996) “Organizational knowledge, learning and memory: three concepts in search of a theory”, Journal of Organizational Change Management, Vol. 9 Iss: 1, pp.63 – 78.

CrossRef

- Jerez Gomez, 2005Je´rez-Go´mez, P., Ce´spedes-Lorente, J. and Valle-Cabrera, R. (2005), “Organizational learning capability: a proposal of measurement”, Journal of Business Research, Vol. 56 No. 6, pp. 715-25

CrossRef

- Jobber, David. “An examination of the effects of questionnaire factors on response to an industrial mail survey.” International Journal of Research in Marketing 6.2 (1989): 129-140.

CrossRef

- Katila, Riitta, and Gautam Ahuja. “Something old, something new: A longitudinal study of search behavior and new product introduction.” Academy of management journal 45.6 (2002): 1183-1194.

CrossRef

- Khong, K. W., & Richardson, S. 2003. Business Process Reengineering In Malaysian Banks And Finance Company. Managing Service Quality. 13(1): 54-71

CrossRef

- Kim, L. (1997). Imitation to innovation: The dynamics of Korea’s technological learning. Harvard Business Press.

- Kireyev, Mr Alexei. Financial reforms in Sudan: streamlining bank intermediation. No. 1-53. International Monetary Fund, 2001.

- Kok Wei Khong, Stanley Richardson, (2003),”Business Process Re-Engineering In Malaysian Banks And Finance Companies”, Managing Service Quality, Vol. 13 Iss: 1 Pp. 54 – 71.

CrossRef

- Lee & Kim, 2015. A Study On The Moderating Effects Of Learning Capabilities On The Types Of Strategic Alliance And Performance-Resource Based Viewadvanced Science And Technology Letters Vol.84 (Business 2015), Pp.45-49

- Lee, H. g., & Clark, T. H. (1996). Market process reengineering through electronic market systems: Opportunities and challenges. Journal of Management Information Systems, 13(3), 113-136.

CrossRef

- Majed Al-Mashari, Mohamed Zairi, (1999),”Business Process Reengineering Implementation Process: An Analysis Of Key Success And Failure Factors”, Business Process Management Journal, Vol. 5 Iss: 1 Pp. 87 – 112

CrossRef

- Martin G Evans, 1985. Organizational Behavior and Human Decision Processes, Volume 36, Issue 3, December 1985, Pages 305-323

- Melville, N, Kraemer, K & Gurbaxani, V 2004, ‘Information Technology And Organizational Performance: An Integrative Model Of It Business Value’, Mis Quarterly, Vol. 28, Pp. 283–322.

CrossRef

- Mohsen Attaran, (2003) “Information Technology And Business‐Process Redesign”, Business Process Management Journal, Vol. 9 Iss: 4, Pp.440 – 458

CrossRef

- Moran, J.W. And Brightman, B.K. (2000), “Leading Organizational Change”, Journal Of Workplace Learning, Vol. 12 No. 2, Pp. 66-74.

- Muhammad Aizat Md Sin*, Mohd. Rizal Razalli. 2015. The Influence Of It Infrastructure In Business Process Reengineering Project Performance In Islamic Banking. Jurnal Teknologi (Sciences & Engineering) 77: 4 (2015) 97–103.

- Neely, A, Gregory, M & Platts, K 1995, ‘Performance Measurement System Design: A Literature Review and Research Agenda’, International Journal Of Operations & Production Management, Vol. 15, Pp. 80–116.

CrossRef

- Nonaka, I., & Takeuchi, H. (1995). The knowledge-creating company: How Japanese companies create the dynamics of innovation. Oxford university press.

- Nunnally, J.L. (1978). Psychometric Theory, 2nd ed., McGraw-Hill, New York, NY.

- O’Neill, P & Sohal, A 1999, ‘Business process reengineering: a review of recent literature’, Technovation, vol. 19, pp. 571–581.

CrossRef

- Olalla, Marta Fossas, Information Technology in Business Process Reengineering, International Advances in Economic Research , Vol. (6), No. (3), EBScohost Databases Business Source Premier, http://search.epent.com. 2000

- Oliver, C. (1997). Sustainable competitive advantage: combining institutional and resource-based views. Strategic Management Journal, 18(9), 697-713.

CrossRef

- Oliver, W.H. (1990), “The Quality Revolution,” Vital Speeches Of The Day, Pp. 625-8.

- Peteraf, M 1993, ‘The cornerstones of competitive advantage: a resource-based view’, Strategic Management Journal, vol. 14, no. 3, pp. 179–191.

CrossRef

- Prieto, I. M., & Revilla, E. (2006). Learning capability and business performance: a non-financial and financial assessment. The Learning Organization, 13(2), 166-185.

CrossRef

- Quinn, R. E., & Rohrbaugh, J. (1983). A spatial model of effectiveness criteria: Towards a competing values approach to organizational analysis. Management science, 29(3), 363-377.

CrossRef

- Ramberg, J.S. (1994), “Tqm: Thought Revolution Or Trojan Horse?,” Or/Ms Today, Vol. 2 No. 4, August, Pp. 18- 24.

- Razalli, M.R. (2008). The consequence of service operations practice and service responsiveness on Hotel performance: Examination of Hotels in Malaysia. Unpublished PhD Thesis, Universiti Sains Malaysia, (USM).

- Ringim, K., Razalli, M., And Hasnan, N., 2012 “The Moderating Effect Of IT Capability On The Relationship Between Business Process Reengineering Factors And Organizational Performance Of Bank”, Journal Of Internet Banking And Commerce, Vol.1 7, No 2, Pp. 1 -21.

- Salimifard, K., Abbaszadeh, M. A., & Ghorbanpur A. 2010. Interpretive Structural Modeling Of Critical Success Factors In Banking Process Re-Engineering. International Review Of Business Research Papers. 6(2): 95-103.

- Samman, Samer, Integrated the Total Quality Management Business Process Reengineering “Model” (Master), University of Jordan, Jordan, 2003.

- Sanchez, C., Soler-Illia, G. D. A., Ribot, F., Lalot, T., Mayer, C. R., & Cabuil, V. (2001). Designed hybrid organic-inorganic nanocomposites from functional nanobuilding blocks. Chemistry of Materials, 13(10), 3061-3083.

CrossRef

- Santos, M. (2005). A urbanização brasileira (Vol. 6). Edusp.

- Sharma et al , 1981 Sharma, S., Durand, M.R. & Gur-Arie, O. (1981). Identification and analysis of moderator variables. Journal of Marketing Research, 18(3), 291-300.

CrossRef

- Sheikh Damanhouri. 2015. ” An Empirical Study On Saudi Arabian Airlines:

- Sherwood-Smith, M. (1994). “People Centred Process Re-engineering: An Evaluation Perspective to Office System Re-design”, in (Glasson et al., 1994), pp. 535-544.

- Sia, S & Neo, B 2008, ‘Business Process Reengineering, Empowerment And Work Monitoring’, Business Process Management Journal, Vol. 14, Pp. 609–628

CrossRef

- Sidikat, A., & Ayanda, M. A. 2008. Impact Assessment of Business Process Reengineering On Organizational Performance. European Journal of Social Sciences. 7(1): 115- 125.

- Sin, M. A. M., & Razalli, M. R. (2015). The Influence of It Infrastructure In Business Process Reengineering Project Performance In Islamic Banking. Jurnal Teknologi, 77(4).

- Tayfur, Mohamed Khair. 2006. “The experience of re-engineering work systems and the overall quality and applied in the PTC in Syria”, unpublished Master, Syria: Aleppo University.

- Teng, J.T.C., Grov9er, V. And Fiedler, K.D. (1994), “Business Process Reengineering: Charting A Strategic Path for The Information Age,” California Management Review, Vol. 36 No. 3, Spring, Pp. 9-31.

- Tranfield, D., Duberley, J., Smith, S., Musson, G., & Stokes, P. (2000). Organizational learning-it’s just routine. Management Decision, 38(4), 253-260.

CrossRef

- Vakola M. & Rezgui Y., (2000): Organizational Learning and Innovation in the Construction Industry, Learning Organization: An International perspective,7(4), 174-183

- Van der Wiele, T., Kok, P., McKenna, R., & Brown, A. (2001). A corporate social responsibility audit within a quality management framework. Journal of Business Ethics, 31(4), 285-297.

CrossRef

- Venkatraman, N. & Ramanujam, V. (1986). Measurement of business performance in strategy research: a comparison of approaches. Academy of Management Review, 11(4), 801-814.

- Wernerfelt, B 1984, ‘A resource-based view of the firm’, Strategic Management Journal, vol. 5, no. 2, pp. 171–180.

CrossRef

- Zairi, M, and Sinclair, D.1995. “Business Process Re-Engineering and Process Management”, Management Decision, Vol.33, No.3, Pp.3-16. Jackson, N.1997. “Business Process Re-Engineering”, Manage.

- Ying Liao Jane Barnes , (2015),”Knowledge acquisition and product innovation flexibility in SMEs”, Business Process Management Journal, Vol. 21 Iss 6 pp. 1257 – 1278

Other:

- Central Bank of Sudan. (2014). Central Bank of Sudan Annual Report and Account as At 31st December.

This work is licensed under a Creative Commons Attribution 4.0 International License.