Introduction

The breakthrough of e-commerce has created an international open market that does not have any kind of geographical constraints. With the start of the twenty first century in cooperation with the IT revolution and the wide use of computers and internet in most fields, the use of the internet as a medium for the execution of the e-commerce operations has widely spread, e-commerce also spread widely facing the new challenge of justifying its operations within mechanical accounting systems in organizations during those incessant rapid changes in information. Resulting of the most significant current problems in the field of e-commerce and their suggested and applied solutions are approached, which tackles the issue of the inevitability of building the legislative structure required for protecting and supporting ones development in the international market especially when performing the commercial exchange processes electronically.

Due to the significant role e-commerce plays in the performance of information systems; the presence of information systems is in general associated with the presence of e-commerce, and as result to the previous state; it is of very big importance for commercial organizations to gather all possible knowledge to keep up with the latest developments in the accounting information systems and its relations with the variety of systems that mainly affects its performance and development.

This paper sets the spotlight on the effects of the use of e-commerce in the development process of accounting information systems. Hence, this problem has more uncertainties in lower scale organizations; the paper goal is to study the effect on medium scale organizations in Middle East, specially, in Jordan.

The commercial transactions which depends on processing of digital data, through open networks whether it was done by individuals and organizations is the main characteristic of e-commerce system. It uses of information technology to perform commercial transactions from selling and buying to physical or digital transfer services. It was defined by the association of control and audit of the Ecommerce information systems as “the processes on which the facilities conduct E-business with clients, suppliers or people who use the internet as a technique that enables them to do so”.

Four different types of e-commerce system are classified based on the dealers’ nature; Business-business, Business organization-consumer, Business Organization-government, and Consumer-government e-commerce transactions.

The business-business (organizations) E-commerce is the most used type of E-commerce, and very widely spread, it is done between business organizations using communication networks, and it includes purchase orders, payments, and receiving of vouchers and payments. The Business organization-consumer e-commerce is also known as e-shopping or retail e-commerce since the deals are done with a consumer directly, what actually happens is that organizations display their products to e-stores on the web, promotes them, then conduct deals with the consumers, it is the least spread type of E-commerce but it is growing widely.

The relationship between the government and the business organizations is clearly presented by business organization-government e-commerce. Wherethe governments’ deals are simply done through the internet, what happens is that they display their needed products or services and the required standards through the internet for business organizations to apply their E-displays so that they can chose a suitable display that agrees to their terms and conditions. This type of e-commerce can be used to settle the corporate taxes. On the other hand, consumer-government e-commerce means that a citizen can conduct and his official papers and bills through the internet simply as paying taxes and paying traffic tickets.

Accounting and auditing divisions must be involved with the E-commerce and it has become of great importance for them learn about it. Hence, the organizations’ financial operations (such as selling) are done by their websites which are directly connected to their accounting information systems. A big change in international trading science and commercial operations mechanisms was made by the e-commerce science and operations. Which made it necessary to the auditors and accountant to comprehend those changes and their effect to the business they do, in addition to legal environmental circumstances concerned with the business (Marcella (1998).

The e-commerce can contribute the quantitative information features, by significantly improving the adequacy features, especially by improving the proper timing subsidiary.

Characteristics of Accounting Information

Adequacy is one of the most critical and essential properties that information must have. It’s defined as that for the information to be compatible with the accounting information users’ requirements, this can also mean the accounting information’s ability to influence a firms administrative decisions and its users ability to predict suitable future events more accurately whether the information was being use internally or externally, but since that problem solving and decision making depend on it directly, it has become of great importance for the internal use. American Accounting Association considered that accounting information cannot be adequate unless it was related to a goal that one is asked to achieve. The subsidiary characteristics of the accounting information adequacy was identified by the Financial Accounting Commission to have time appropriate, ability to predict, regressive feed-back, reliability, honesty in the presentation information, impartiality, verifiability, subsidiary characteristics, comparability, and coherence.

Conventionally, the AIS i1s made up of several subsystems operating together coherently to supply all parties in an economic unity with needed information.

It can also be defined to be a component of an administrative organization that is specialized in collecting, tabulating, processing, analyzing and delivering of the proper information for decision making to the outside parties.

Accounting information systems are built up of multiple components to accomplish a certain objective that was originally established. This component contains at first the evidentiary papers and documents: which supports any financial transaction happened within the organization. Also, the data base is the components that are used to store any financial data for use in accounting transactions, in addition to the Proper computer software for data processing. Also, one of the basic components is the written and drawn accounting procedures to keep track of the sequence of the organizations financial operations. In addition to the above components, the personnel, or man power, which means employees that have the ability to use one or more accounting systems, represents very basic issue with the cooperation of electronic gear and proper communications technology.

It is important for an accounting information system to have certain features which qualify to be efficient (Al-Rawi, 2009). The high accuracy of AIS is the most needed feature, with the ability to fast processing the financial data. It must be able to supply the essential accounting information to the functional performance in the right time for it to make up a decision for choosing ascertain variable from an available group of variables.

Efficient AIS must be able to supply the essential information for supervision and assessment of the organizations financial activities, to the administration. Also, the essential information should be capable to be supplied for achieving critical tasks which means short, mid and long term planning for the organizations future business, to the administration, and recollection of any quantitative descriptive information stored in its database fast and accurately when needed.

When designing an accounting information system, designers and analysts are working on a system that must be familiar with certain characteristics which can represent the key principles in designing an effective accounting information system. The most important characteristics that should be considered in AIS design is that, the data preparing cycle of the accounting information system, the applied environment and AIS network, with comprehensive consideration of the main purposes AIS targeted application.

The criteria that could be used to measure the reliability, efficiency and usability of the AIS ensures that, it should performs many challengeable tasks with high adequacy, that starts by data collection and store with the activities and operations of the organization, effectively. Then, Processing, sorting, summarizing, and classifying of these data, and generating essential information for decision making to provide the users . And also, to perform the supervision principle.

Objectives

This paper studies a middle-eastern sample of non-larger organizations, which have an overhead that could be caused by applying a non-efficient accounting information system. The Jordanian companies that been subjected to this study is the medium scale organizations which locates in med way between larger transactions that substitute the cost and complexity of the AIS and between the overhead of AIS and e-commerce systems installation, license, and operation costs.

This paper aims to study the targeted sample that works on both, e-commerce and AIS in parallel and thus, estimate the effect of e e-commerce on the process of accounting information systems design, and to estimate the forecasted effect of e-commerce on the accounting information systems inputs.

The processing operation in AIS concatenation with e-commerce transactions is targeted to be estimated in this paper also, with that effect on output of AIS with respect to internal control operations, audits, and managerial decision making process. While the information security of both; e-commerce and AIS, could be subjected to be affected by each other, and the legal operations of internal control and audits give this criterion some transparency, this milestone point will be discussed in later section. And the collected information related to the transactions and control events of each type will be discussed also.

Hypothesis

Objectives of this paper are firstly achieved by designing a reasonable representing hypothesis, in the form of questionnaire. That questionnaire was surveyed by the study sample of this paper, which are the med-scale business organizations in Jordan market. The results of this hypothesized questionnaire are used to analyze the research problem and study the criteria, measurements, and resulted decisions the hypothesized questions are described in the follow.

Hypothesis: The use of e-commerce is affected accounting informational systems methodology that used in most organization.

Hypothesis: The use of e-commerce does not affect the design of accounting structure of the organization

Hypothesis: The functional processes in AIS are functions of e-commerce dependability on internal control strategies

Hypothesis: The income always increases with adaptation of AIS based e-commerce

Hypothesis: The flow of decision making changes when applying e-commerce with integrated AIS for more trust, while an e-commerce without proper AIS makes the managerial decisions more critical.

Hypothesis: Applying an e-commerce does affect the data security in accounting information systems

Related work

[Muhannad, 2013] study and demonstrated the effect of e-commerce on accounting information systems considering the both; e-commerce and the accounting information system as the most tools that is used to develop the world of business. The society of Jordan firm was considered to be the case study, but without discrimination between the scale of organizations. The scale of organizations in Jordan easily varies from few number of employees (i.e. less than 10) to hundreds of thousands employees. So, this paper ignored important criteria in its study and results. Also, the single relation between the two parts of science and applications those studied in that paper is the cost efficiency. So, that paper needs to be supported with other researches – like this paper – to generalize the results and to specialize the case studies and support the extracted and analytical results with rigid scientific research decisions.

[Khalil, 2012] Supposes that, there are no known relation between the e-commerce and the accounting information systems in a single case study, which is a large bank. But the study results show that the AIS are affected by the use of e-commerce firms. That paper demonstrated the security issues with access control security in terms of AIS and e-commerce. That paper is limited and takes a single case study with a non reasonable hypothesis that assumed the case study to be generalized, whit it in fact is not. Also, that paper doesn’t demonstrate a realistic model for different scales organizations.

[Adel, 2012] also demonstrated a single case study to show the effect of e-commerce on an accounting information system. As [Khalil, 2012] The author of [Adel, 2012] takes one bank as a case study, to analyze the reliability of AIS in the applications that deal with e-commerce as a basic operation of its transactions. The hypothesis and study sample of that paper were not faire. It stands on non-practical hypothesis that assumed ideal internet and computer technology based transactions, ignoring all effects of non-human based decision making processes.

In contrast, this paper aims to study generalized firm of organizations in Jordan market that is the medium scale organization. The study is being done in terms of cost, reliability, security, and human in dependability, for the very constrained complex business model organizations.

Methodology

For data collection; a questionnaire on the effect of the use of e-commerce on the accounting information systems of these organizations was designed and distributed to a number of organizations, the questionnaire proposed the hypothesis those demonstrated in section-4.

The questionnaire was made taking into account the recommendations of AIS support organizations and some related researches. The questionnaire was targeted the financial and managers of organization, IT managers, audits, and executive managers. It collected with direct interview with the responsible peoples in the sample study organizations.

The study sample was involved 170 organizations in Jordan that considered being medium scale organizations. The result of questionnaire was collected within one month and the data entry process resulted a useful data for processing and analysis.

The data were processed and analyzed using MATLAB. The results of analysis are demonstrated in the next section. The problem definition that presented in the first section of this paper is studies, analyzed, and its results were demonstrated in the next section too.

Results

This paper looks at the effect of e-commerce on the development of accounting information systems AIS in organizations. The survey is Jordan organizations since the countries like Jordan has its Organizational companies to work in very dynamic work order.

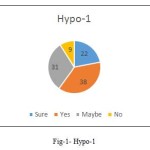

The figure above represents the results we got for our fist hypothesis, 22% of the sample assured our 1st hypothesis that The use of e-commerce has affected accounting informational systems methodology that used in most organizations, 38% said yes, 31% said maybe while 9% had denied it.

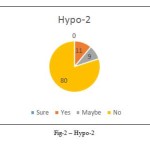

None of the sample had assured our 2nd hypothesis which suggests that the use of e-commerce does not affect the design of accounting structure of the organization, 11% said yes, 9% said maybe while 80% had denied it.

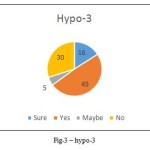

16% of the sample had assured our 3rd hypothesis which suggests that the functional processes in AIS are functions of e-commerce dependability on internal control strategies, 49% said- yes, 5% said maybe while 30% had denied it.

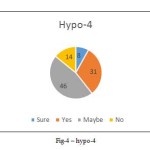

8% of the sample assured our 4th hypothesis which says that the income always increases with adaptation of AIS based e-commerce, 31% said yes, 46% said maybe while 14% had denied it.

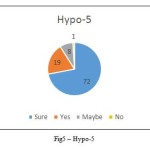

72% of the sample assured our 5th hypothesis which suggests that the flow of decision making changes when applying e-commerce with integrated AIS for more trust, while an e-commerce without proper AIS makes the managerial decisions more critical, 19% said yes, 8% said maybe while 1% had denied it.

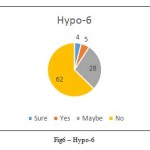

4% of the sample assured our 6th hypothesis which suggests that Applying an e-commerce does affects the data security in accounting information systems, 5% said yes, 28% said maybe while 62% had denied it.

The results above support the assumption that there is a positive effect of e-commerce on AIS is positive, hence the increase in efficiency, competence, and financial stability of organizations.

In comparison with the related works those described in section-5, this paper has many keynotes; this paper is generalized for all medium scale organizations, so, it is applicable on both [Adel, 2012], and [Muhannad, 2013]. Also, [Khalil, 2012] states that, the e-commerce affects the use of AIS in his case study. But as shown in the results, the AIS firm adoption supports the process and e-commerce stability, security, and controllability. Even though, many point should be spotted and the control strategy needs to be more accurate, more specific, and completely workarounds free, but the use of AIS cooperation with e-commerce systems increase the reliability and the trust of audit, and internal control strategies. This result was not clear in [Adel, 2012], and contradictory with the [Khalil, 2012].

Conclusion

The development process of accounting information systems is significantly affected by the existence of electronic commerce. It also proved that there is a very strong connection between e-commerce and the efficiency, reliability, and information security of the accounting information systems in organizations, the reliability and efficiency of accounting information systems was improved significantly by the use of e-commerce, in most cases; it increases the data processing capability of an organization (reduce errors, verify data, data protection and security, etc.).

The application of e-commerce through accounting information systems has a significant effect on the organizations capability to reduce costs and improve performance.

The use of electronic commerce had significantly improved Efficiency, reliability, and data security of accounting information systems in organizations.

References

- Muhannad Akram Ahmad, Effect of ECommerce on Accounting Information System, Computerization Process and Cost Productivity, American Journal of Computer Technology and Application Vol. 1, No. 1,February 2013, PP: 01 – 06, ISSN: 2327- 2325

- Khalil Mahmoud AL-Refaee, The Effect of E-Commerce on the Development of the Accounting Information Systems in the Islamic Banks, American Journal of Applied Sciences 9(9): 1479-1490 (2012)ISSN 1546-9239, © 2012 Science Publication

- Adel M Qatawneh, The Effect of Electronic Commerce on the Accounting Information System of Jordanian Banks, International Business Research, Vol. 5, No. 5; (2012).158 ISSN

- Al-Helo, B., Effect of Using Information Technology System on the Comprehensive Banking Services in the Jordanian Banks from the Perspective of the Banking Leaderships. M.Sc Thesis, AL-Albeet University, Jordan (2000).

- AL-Qudah, G., The impact of accounting information systems on the effectiveness of the internal control in Jordanian banks, electronic version. Interdisciplinary Journal of Contemporary Research In Business, 2(9): 365-377 (2011).

- Al-Rawi, H., Accounting information systems and the organization. Culture 8 AHMAD et al., Orient. J. Comp. Sci. & Technol., Vol. 7(1), 01-08 (2014) Library for Publishing and Distribution, Jordan (2009).

- Whelan, E., Exploring knowledge exchange in electronic networks of practice. Journal of Information Technology, 22(1): 5-12(2007).

CrossRef

- Purwadi, P., Advantages of web services in E-Business, A large scale empirical study. Working paper. MITsloan School of management (2008).

- Turban, E., King, D., Lee, J., Liang, T., and Turban, D. C., Electronic Commerce a Managerial Perspective. New Jersey: Prentice Hall (2010).

- AICPA/CICA., Privacy frame work including the AICPA/CICA trust service privacy principles and criteria, issued by the assurance services executive committee of the AICPA and the assurance services development board of the CICA (2004).

- Barczak, G., Sultan, F., & Hultink, E. J., Determinants of IT usage and new product performance. The Journal of Product Innovation Management, 24(6): 600-613 (2007).

CrossRef

- Davenport, T. H., Putting the enterprise into the enterprise system. Harvard business review, 76(4): 121-131 (1998).

- Lymer, A., &Debreceny, R., The Auditor and corporate reporting on the internet: challenges and institutional responses. International journal of auditing, 7: 103-120 (2003).

CrossRef

- Romney, M. B., & Steinbart, P. J., Accounting information system. New Jersey: Prentice Hall (2012).

- Zikmund, W. G., Business research methods (7th ed.). Thomas south-western (2003).

This work is licensed under a Creative Commons Attribution 4.0 International License.